Assessing the Barbados SSB Tax

Assessing the Barbados SSB Tax

Evaluating and guiding policy decision-making in the Caribbean on the taxation of Sugar Sweetened Beverages

There is increasing international interest in using fiscal measures on food and non-alcoholic beverages as preventive measures for NCDs. A specific recommendation is to increase the tax on sugar sweetened beverages (SSBs), so that they are more expensive that non-sugar sweetened beverages. In the June Budget Statement in 2015 the Government of Barbados announced a 10% tax on SSBs, and this came into effect on September 1, 2015. The aims of the study are to evaluate the potential impact of a tax on SSBs in Barbados, develop methods that can be applied in other Caribbean countries to evaluate the impact of a tax on SSBs, and inform policy decision making on SSB taxes within the Caribbean region.

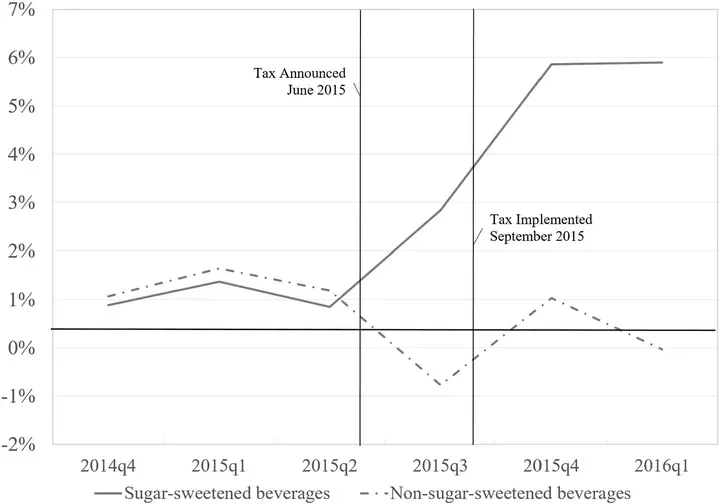

Prior to the tax, year-on-year price growth of SSBs and non-SSBs was very similar (approximately 1%). During the quarter in which the tax was implemented, the trends diverged, with SSB prices growing by almost 3% while prices of non-SSBs decreased slightly. The growth of SSB prices outpaced non-SSBs prices in each quarter thereafter, reaching 5.9% growth compared to <1% for non-SSBs.

Future analyses will assess the trends in prices of SSBs and non-SSBs over a longer period and will integrate price data from additional sources to assess heterogeneity of post-tax price changes. A continued examination of the impact of the SSB tax in Barbados will expand the evidence base available to policymakers worldwide in considering SSB taxes as a lever for reducing the consumption of added sugars at the population level.

Download our article on methods for assessing SSB taxation.

Download our article on price trends after SSB introduction.

Ian Hambleton

Professor of Biostatistics and Informatics

My research themes include data handling technologies, systematic review methods, health inequalities, health in small islands.