Using nutritional survey data to inform the design of sugar-sweetened beverage taxes in low-resource contexts: a cross-sectional analysis based on data from an adult Caribbean population.

Abstract

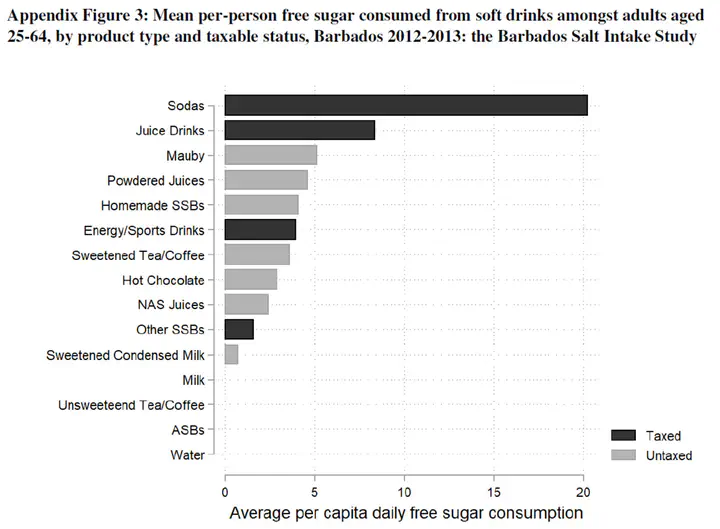

OBJECTIVE: Sugar-sweetened beverage (SSB) taxes have been implemented widely. We aimed to use a pre-existing nutritional survey data to inform SSB tax design by assessing: (1) baseline consumption of SSBs and SSB-derived free sugars, (2) the percentage of SSB-derived free sugars that would be covered by a tax and (3) the extent to which a tax would differentiate between high-sugar SSBs and low-sugar SSBs. We evaluated these three considerations using pre-existing nutritional survey data in a developing economy setting. METHODS: We used data from a nationally representative cross-sectional survey in Barbados (2012-2013, prior to SSB tax implementation). Data were available on 334 adults (25-64 years) who completed two non-consecutive 24-hour dietary recalls. We estimated the prevalence of SSB consumption and its contribution to total energy intake, overall and stratified by taxable status. We assessed the percentage of SSB-derived free sugars subject to the tax and identified the consumption-weighted sugar concentration of SSBs, stratified by taxable status. FINDINGS: Accounting for sampling probability, 88.8% of adults (95% CI 85.1 to 92.5) reported SSB consumption, with a geometric mean of 2.4 servings/day (±2 SD, 0.6, 9.2) among SSB consumers. Sixty percent (95% CI 54.6 to 65.4) of SSB-derived free sugars would be subject to the tax. The tax did not clearly differentiate between high-sugar beverages and low-sugar beverages. CONCLUSION: Given high SSB consumption, targeting SSBs was a sensible strategy in this setting. A substantial percentage of free sugars from SSBs were not covered by the tax, reducing possible health benefits. The considerations proposed here may help policymakers to design more effective SSB taxes.